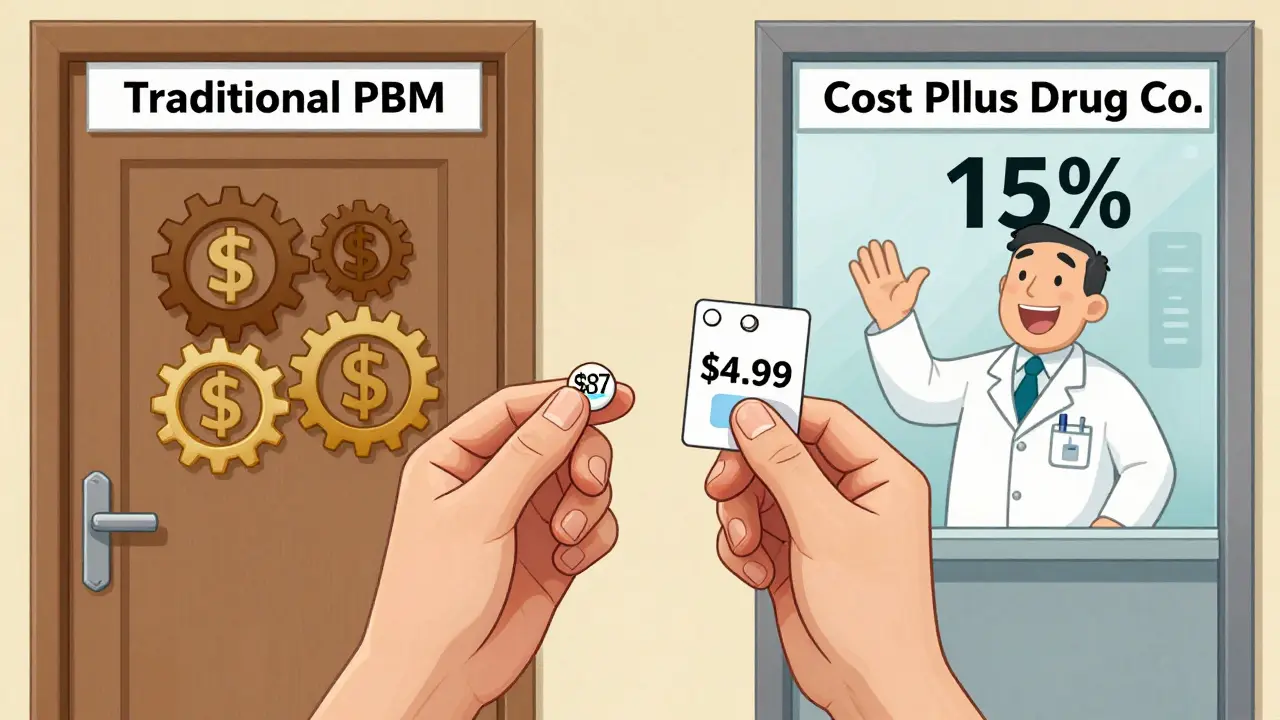

Most people assume that generic drugs are automatically cheap. But if you’ve ever checked your insurance statement after filling a prescription, you know that’s not always true. A generic blood pressure pill might cost $87 through your plan, but only $5 if you pay cash. What’s going on? The answer lies in how insurers buy these drugs-through bulk buying and tendering. These aren’t just buzzwords. They’re the backbone of how health plans save billions every year, and sometimes, they’re the reason you’re still overpaying.

How Bulk Buying Works for Generic Drugs

Bulk buying means insurers and pharmacy benefit managers (PBMs) don’t shop for drugs one prescription at a time. Instead, they group thousands-sometimes millions-of prescriptions into one giant order. Think of it like buying toilet paper in a warehouse club. The more you buy, the lower the price per unit. With generics, that math works even better.

When a patent expires on a brand-name drug, multiple manufacturers can start making the same pill. That’s when competition kicks in. One company might sell the drug for $10 per pill. Another, with lower production costs, might offer it for $2. If an insurer signs a contract with that second company for 10 million pills a year, the price can drop even further-sometimes below $1 per pill. That’s bulk buying in action.

According to the Association for Accessible Medicines, generics made up 90.7% of all prescriptions filled in the U.S. in 2023, but only accounted for 17.3% of total drug spending. That’s because bulk purchasing drives prices down hard. A single new generic drug entering the market can save over $1 billion in its first year, as seen with drugs like lacosamide and bortezomib. The savings aren’t theoretical-they’re real, and they’re massive.

Tendering: The Auction System Behind the Scenes

Bulk buying alone doesn’t guarantee the lowest price. That’s where tendering comes in. It’s essentially a reverse auction. Insurers or PBMs issue a request for bids from generic drugmakers. They say: “We need 5 million tablets of atorvastatin this year. Who can deliver it cheapest?”

Companies respond with their lowest possible price. The insurer picks the bid that offers the best combination of price, reliability, and quality. Contracts typically last one to three years. The winner gets guaranteed volume. In return, they agree to supply at rock-bottom prices.

This system works best when there are multiple manufacturers. If five companies can make the same generic, competition keeps prices low. But if only two or three can produce it, the insurer loses leverage. That’s why some drugs still cost too much-even though they’re generic. The FDA’s Drug Competition Action Plan found that 80% of certain generic drugs are made by just three manufacturers. That’s not competition. That’s a bottleneck.

Why Your Insurance Still Charges You Too Much

Here’s the twist: even when insurers save millions through bulk buying and tendering, you might not see it. Why? Because many PBMs use a hidden trick called “spread pricing.”

Spread pricing means the PBM tells your insurer they paid $3 for a drug. But they actually paid $1.50. The $1.50 difference? That’s their profit. They don’t share it with you. Your copay stays the same, even though the drug cost half as much as what your plan was told.

A 2022 study in JAMA Network Open found that plan sponsors-like your employer or health insurer-often don’t even know which generic drugs are driving up costs. Some high-cost generics have fewer manufacturers, making them harder to replace. So insurers keep paying more, and you pay more too.

One Reddit user, u/PharmaPatient, shared that their generic medication cost $87 through insurance-but only $4.99 when paid cash at a direct-to-consumer pharmacy. That’s not a glitch. That’s the system working exactly as designed-for the middlemen, not for you.

Transparent Models Are Changing the Game

Not all insurers play this game. Some are cutting out the middleman entirely.

Mark Cuban’s Cost Plus Drug Company, for example, charges a flat 15% markup on the cost of the drug plus a $3 pharmacy fee. No spreads. No hidden fees. No formulary games. Their prices are often 75-91% lower than retail pharmacy prices, according to a 2023 NIH study. Blueberry Pharmacy, another transparent model, reports average customer savings of $231 per prescription for expensive generics.

Even Medicare is moving toward transparency. In January 2024, the Centers for Medicare & Medicaid Services required all Part D plans to disclose how much they pay pharmacies for drugs. For the first time, beneficiaries can see whether their plan is getting a fair deal.

And it’s working. A 2023 report from Navitus Health Solutions showed that employers using transparent PBM models saved 22% on generic drug costs compared to traditional ones. That’s not a small win-it’s life-changing for people on multiple medications.

What You Can Do Right Now

You don’t need to wait for your insurer to fix the system. You have power.

- Check GoodRx or SingleCare before filling any generic prescription. You’ll often find prices lower than your insurance copay.

- Ask your pharmacist: “Is there a cheaper generic version?” Sometimes, two generics exist-one costs $5, another $20. They’re chemically identical.

- Request a formulary review from your employer or insurer. Ask: “Which generics are costing us the most? Are we using the lowest-cost option?”

- If you’re on Medicare, compare Part D plans every year. The cheapest plan in 2024 might not be the cheapest in 2025.

One GoodRx user reported saving $32 a month on three generics just by ignoring insurance and using coupons. That’s $384 a year. For someone on five medications? That’s over $600. That’s not a drop in the bucket. That’s a rent payment.

The Bigger Picture: Savings, Shortages, and Systemic Flaws

Bulk buying and tendering save the U.S. healthcare system over $445 billion a year in generic drug costs. That’s money that goes back into care, research, and lower premiums. But there’s a dark side.

When prices get pushed too low, manufacturers quit. In 2020, albuterol inhalers disappeared from shelves because the price dropped below production cost. Eighty-seven percent of hospitals reported shortages. The same thing happened with antibiotics, thyroid meds, and even insulin generics.

And while the FDA approved 1,200 new generics in 2022, the system still favors big players. Only a handful of companies produce most generics. That limits competition. That limits savings.

What’s needed isn’t just more buying. It’s smarter buying. Regular reviews. Transparent pricing. And a shift away from models that reward high prices over real savings.

The Association for Accessible Medicines says annual savings from generics could grow by $127 billion over the next decade-if we fix how we buy them. That’s not a pipe dream. It’s just good procurement.

Why do some generic drugs cost more than others if they’re the same?

Even though two generic drugs have the same active ingredient, they can come from different manufacturers with different production costs. Some companies use cheaper facilities or bulk raw materials, letting them offer lower prices. Insurers often choose the lowest bidder, but if only one or two companies make a drug, there’s no competition-and prices stay high. Some generics also come in different formulations (like extended-release), which can cost more even if they’re therapeutically equivalent.

Can I save money by paying cash instead of using insurance for generics?

Yes, often dramatically. In 2020, 97% of cash payments for prescriptions were for generic drugs, even though cash payments made up only 4% of all prescriptions. Why? Because insurance plans often have high copays or deductibles that don’t reflect the actual cost of the drug. Paying cash at pharmacies like Costco, Walmart, or Cost Plus Drug Company can cut your cost by 75% or more. Always compare cash prices with your insurance copay before filling a prescription.

Do all insurers use tendering and bulk buying?

Most large insurers and pharmacy benefit managers (PBMs) do. The big three-OptumRx, Caremark, and Express Scripts-manage pharmacy benefits for about 280 million Americans. But not all of them use transparent models. Many still rely on spread pricing, where the PBM keeps the difference between what they pay the pharmacy and what the insurer pays them. Smaller insurers or self-funded employer plans are more likely to use transparent, competitive bidding because they have more control over their contracts.

What’s the difference between a generic and a brand-name drug?

A generic drug contains the same active ingredient, dosage, and route of administration as the brand-name version. It must meet the same FDA standards for safety, strength, and quality. The only differences are in inactive ingredients (like fillers or dyes) and packaging. Generics are not “weaker” or “lower quality.” They’re the same medicine, sold at a fraction of the price-often 80-90% cheaper.

Why don’t insurers always pick the cheapest generic?

Sometimes, they’re not told which one is cheapest. Many PBMs don’t disclose pricing details to insurers. Other times, the cheapest option has supply issues or a history of quality problems. But more often, it’s because the PBM benefits from a higher-priced drug. If the PBM gets a rebate or kickback from the manufacturer of a more expensive generic, they’ll keep it on the formulary-even if a cheaper, equally effective option exists. That’s why regular audits of formularies are critical.

Adebayo Muhammad

Let’s be real-this isn’t about healthcare, it’s about power. Bulk buying? Tendering? These are just fancy words for monopolistic collusion disguised as efficiency. The system doesn’t save money-it redistributes it upward, from patients to middlemen with MBA’s and offshore bank accounts. And don’t get me started on spread pricing: it’s not a loophole-it’s a heist. The FDA approves generics, but the PBM decides who wins? That’s not capitalism. That’s feudalism with spreadsheets.

And yet, nobody calls it out. We’re all just… accepting it. Like it’s natural. Like the sky is blue. But the sky isn’t blue-it’s a corporate illusion. We’re being gaslit by pharmacy benefit managers who speak in bullet points and think ‘transparency’ is a marketing campaign. Wake up. This isn’t economics. It’s extortion dressed in white coats.

Pranay Roy

Actually, you’re missing the bigger picture. The entire system is engineered by Big Pharma to keep generics low-cost so they can keep hiking prices on the 3% of drugs that still have patents. The real villain isn’t the PBM-it’s the patent system. They let generics in just enough to create the illusion of competition, then they patent new formulations, new delivery methods, new packaging. It’s all a distraction. Meanwhile, you’re overpaying for insulin because they changed the vial size and called it ‘improved.’

And yes, paying cash works-but only if you’re not on Medicaid or Medicare. The system is rigged to punish the poor. The rich get Cost Plus Drug Co. The poor get $87 copays and a prayer.

Joe Prism

It’s not broken. It’s optimized-for someone else.

Generics save billions. That’s undeniable.

But the savings aren’t passed on. That’s the flaw.

Transparency isn’t a bonus. It’s the baseline.

And yes-paying cash often beats insurance. Always check.

Bridget Verwey

Oh honey. You think this is about drugs? Nah. This is about who gets to play the game.

You’ve got a PBM that acts like a black box, an insurer that doesn’t know what they’re paying for, and a patient who’s just trying to not pass out from high blood pressure.

Meanwhile, someone’s sipping a $12 latte in a Manhattan office, counting how much they pocketed from your $87 copay.

Don’t rage. Just go to GoodRx. Then tell your boss. Then tell your senator. Then tell your grandma. Then do it again.

Change doesn’t come from outrage. It comes from repetitive, annoying, relentless action.

Andrew Poulin

Stop overcomplicating this. Cash is cheaper. Use it. End of story.

Insurance is a scam. PBMs are parasites. You don’t need a PhD to get your meds cheap.

Go to Walmart. Pay $4. Walk out. Done.

Weston Potgieter

So the system’s rigged. Big whoop. Welcome to America. We’ve got free markets and 12-step programs for the people who can’t afford insulin.

Some genius at the FDA approved 1200 generics last year. Meanwhile, people are dying because the only guy who can make a thyroid med is in a basement in Bangalore and his machine broke.

It’s not a conspiracy. It’s capitalism. It’s messy. It’s ugly. It’s real.

And you? You’re mad because you got hosed on a $87 copay? Honey. Try living on $15k a year and see how many times you even check the price.

Vikas Verma

Strategic procurement in pharmaceutical supply chains requires robust vendor diversification and risk mitigation protocols. The current tendering mechanisms are suboptimal due to concentration risk in manufacturing ecosystems. Only 3 manufacturers per generic = systemic vulnerability.

Recommendation: Implement multi-sourcing mandates for Tier-1 therapeutics. Align with WHO Essential Medicines List benchmarks. Introduce dynamic pricing algorithms based on real-time supply chain metrics.

Without structural intervention, we risk catastrophic shortages. The economic savings are significant, but not sustainable.

Sean Callahan

so like… i just found out my insurance paid $72 for my blood pressure med… but i paid $87… and then i checked goodrx… it was $3.50???

wait wait wait… so i’ve been paying 20x more… for 2 years…

my therapist is gonna have a field day with this

why does this feel like betrayal

Amina Aminkhuslen

Y’all are missing the forest for the trees. This isn’t about drugs. It’s about control. Who owns your health? The doctor? The pharmacist? The insurer? Or the guy in a suit who got a 12% kickback from the manufacturer of the $20 generic instead of the $5 one?

It’s not a market failure. It’s a moral failure. And nobody wants to talk about that. Because then they’d have to look in the mirror.

And honestly? I’m tired of being complicit.

Tim Hnatko

I work in a clinic. We have patients who choose between insulin and rent. We have patients who split pills because they can’t afford the full dose. We have patients who cry when they find out their $87 copay is actually $4 cash.

This isn’t a policy debate. It’s a human crisis.

Yes, the system is broken. But we can fix it. One patient. One conversation. One GoodRx search at a time.

Don’t rage. Help.

Joey Pearson

You can do this. Seriously. Go to GoodRx. Check your meds. Talk to your pharmacist. Ask if there’s a cheaper version. You’d be shocked how often the answer is yes.

And if you’re on Medicare? Switch plans every year. It takes 10 minutes. Could save you hundreds.

You’ve got more power than you think.

Roland Silber

Here’s what nobody says: the reason cash is cheaper is because pharmacies are absorbing the cost to get you in the door. They’re making money on foot traffic-lattes, snacks, OTC meds.

So when you pay cash, you’re not ‘beating the system.’ You’re subsidizing the pharmacy’s business model.

It’s not evil. It’s just… weird.

But hey-if it works, use it. Just know why.

Patrick Jackson

Imagine this: you’re a drugmaker. You spent $1B developing a brand-name drug. Now the patent expires. Suddenly, 12 companies are making the same pill. You can’t compete. So you… wait. You wait until only 3 are left. Then you buy one. Then you raise prices. Then you patent the *color* of the pill.

That’s not innovation. That’s a magic trick.

And we’re all clapping.

😭

Ferdinand Aton

Actually, paying cash is a myth. I tried it. The cash price was higher than my insurance. Turns out my plan had a special deal with my local CVS. So yeah-sometimes insurance wins.

Don’t believe everything you read on Reddit.